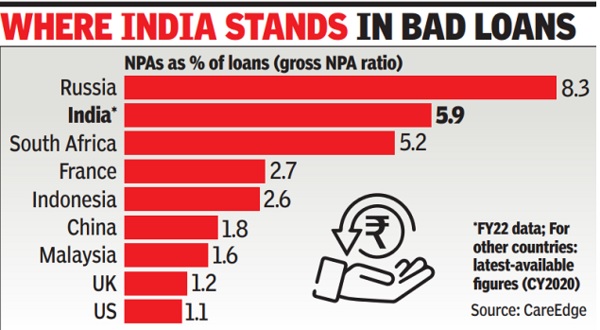

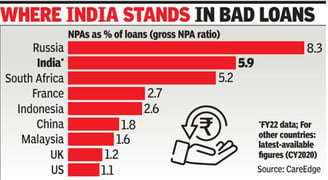

The Challenges Facing the Banking System in India: A Closer Look at NPA Loans and Corporate Defaults

The banking system in India has been facing significant challenges in recent years, with a growing number of non-performing assets (NPAs) and corporate loan defaults. These issues have had a profound impact on the overall health of the banking industry and the economy as a whole. In this article, we will delve into the reasons behind the current state of the banking system in India and explore the factors contributing to the high number of NPAs and corporate loan defaults.

The Rise of Non-Performing Assets (NPAs)

Non-performing assets, commonly known as NPAs, refer to loans that have stopped generating income for banks due to default or non-payment by borrowers. The alarming increase in NPAs is a major concern for the banking sector in India. Several factors have contributed to this rise:

Economic Slowdown: The Indian economy has witnessed a slowdown in recent years, impacting various sectors. This has led to a decrease in business profitability, making it difficult for borrowers to repay their loans.

Weak Credit Appraisal Practices: In some cases, banks have been lenient in their credit appraisal practices, leading to inadequate assessment of borrowers' repayment capabilities. This has resulted in loans being extended to borrowers who were unable to repay them.

Insufficient Risk Management: Some banks have faced challenges in effectively managing risk associated with lending. Inadequate monitoring and follow-up on loans have contributed to the increase in NPAs.

Political and Regulatory Factors: Political and regulatory factors have also played a role in the rise of NPAs. Loan waivers and political interference in the lending process have impacted the ability of banks to recover loans.

Corporate Loan Defaults:

In addition to NPAs, the banking system in India has also witnessed a significant number of corporate loan defaults. Corporate loan defaults occur when companies are unable to fulfill their repayment obligations. Here are some reasons behind this phenomenon:

Business Failures: Economic downturns, market volatility, and poor business strategies have led to the failure of many companies. When businesses fail, they are often unable to repay their loans, resulting in defaults.

Corporate Governance Issues: Weak corporate governance practices can contribute to loan defaults. Lack of transparency, mismanagement, and diversion of funds are some of the governance issues that have plagued certain companies.

Lack of Accountability: In some cases, there has been a lack of accountability on the part of borrowers and lenders. This has allowed borrowers to default on their loans without facing adequate consequences.

Legal Challenges: Lengthy legal processes and inadequate bankruptcy frameworks have hindered the recovery of defaulted loans. This has further exacerbated the problem of corporate loan defaults.

The banking system in India is taking steps to address these challenges and improve the overall condition of the industry. The government has implemented various measures, including the Insolvency and Bankruptcy Code, to expedite the resolution of NPAs and corporate defaults. Banks are also focusing on strengthening their risk management practices and enhancing credit appraisal mechanisms.

In conclusion, the banking system in India is facing significant challenges due to the rise in NPAs and corporate loan defaults. Economic slowdown, weak credit appraisal practices, insufficient risk management, political and regulatory factors, business failures, corporate governance issues, lack of accountability, and legal challenges are some of the key factors contributing to this situation. It is crucial for all stakeholders, including banks, borrowers, regulators, and the government, to work together to address these issues and restore the health of the banking system.